No Surprises Act

I got a surprise medical bill from the ER. What now?

By BillBusted • Published May 6, 2026 • 9 min read

An unexpected bill after an emergency visit is one of the most common — and most legally contested — situations in American healthcare. Federal law passed in 2022 gives you real protections. Here is how to use them.

What a surprise ER bill actually is

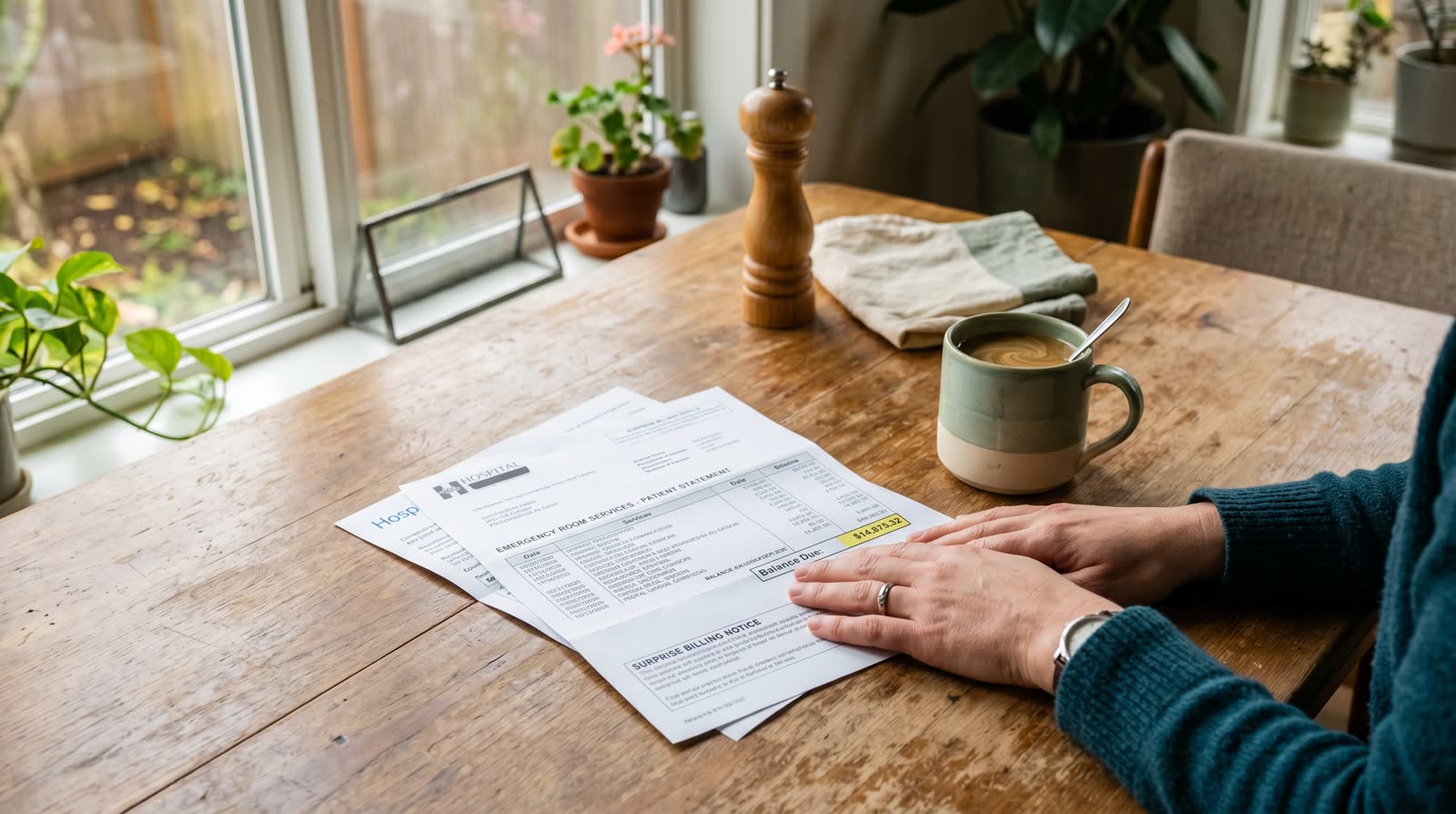

A surprise medical bill — sometimes called a balance bill — happens when you receive care from a provider who is outside your insurer's network, and that provider charges you the difference between what your insurer paid and the provider's full rate. In an emergency, you typically have no opportunity to check network status. You go to the nearest ER, and weeks later a bill arrives from an emergency physician group you have never heard of.

This scenario is common enough that Congress addressed it specifically. The No Surprises Act, which took effect January 1, 2022, made most forms of surprise balance billing from emergency providers illegal under federal law.

The CFPB reported in 2024 that up to 49% of all medical bills contain at least one error — and surprise ER bills are among the highest-error categories, because they often involve multiple billing entities (the facility, the physician group, radiology, anesthesiology) each billing separately.

The No Surprises Act: what it covers

The No Surprises Act (NSA) is a federal law that limits what you can be charged in three specific situations:

Emergency services at any facility

If you receive emergency services — defined by the reasonable layperson standard, meaning any condition you reasonably believed required immediate care — your out-of-pocket cost cannot exceed your in-network cost-sharing amount, regardless of whether the treating provider is in or out of network. You pay your normal in-network deductible, copay, and coinsurance. Period.

Out-of-network providers at in-network facilities

Even after the emergency phase ends, if you are admitted to an in-network hospital and receive non-emergency services from an out-of-network provider (an assistant surgeon, a consulting specialist, a hospitalist), your cost is limited to your in-network amount — unless you received and signed an advance consent form acknowledging the out-of-network provider and the estimated cost. Verbal consent at intake does not count.

Air ambulance services

Air ambulance is covered by NSA balance-billing protections as well, with the same in-network cost-sharing cap. Ground ambulance is notably excluded and remains a significant gap in federal protection as of 2026.

Our Surprise Medical Bill Help page covers the full scope of NSA protections with scenario-specific guidance.

What to verify before you pay or dispute

Before taking any action, gather and confirm these four things:

Confirm the date of service was a genuine emergency

The NSA applies to emergency services. If the visit was a scheduled procedure or a follow-up, different rules may apply. An ER visit for acute chest pain — emergency. A scheduled outpatient procedure at an ambulatory surgical center — may not be covered the same way.

Identify every biller

An ER visit can generate bills from the hospital facility, the emergency physician group (often contracted separately), radiology, lab, and anesthesiology. Request a full itemized bill from each entity that sent you a statement. Each biller's network status matters independently.

Check your EOB

Your Explanation of Benefits will show what your insurer paid and what it says you owe. Compare this to the bill you received. If the bill exceeds the EOB's patient-responsibility amount, that is a likely violation of your plan contract and possibly federal law. See our bill vs EOB mismatch guide for how to read the discrepancy.

Identify your plan type

The NSA applies to most private insurance plans — fully insured employer plans, ACA marketplace plans, individual and small-group plans, and self-funded employer plans. Medicare Advantage has its own network rules. Confirm your plan type on your insurance card or by calling the member services number on the back.

Who is covered — and who is not

The NSA covers most commercially insured patients, but there are gaps worth knowing:

- Covered: Fully insured employer plans, ACA marketplace plans, individual/small-group plans, self-funded employer plans, Federal Employee Health Benefit plans.

- Partially covered: Medicare Advantage (has its own network and balance-billing rules).

- Not covered by NSA: Original Medicare (has its own assignment rules), Medicaid, VA care, TRICARE, and some grandfathered plans. Many states have additional protections that may fill gaps.

- Not covered for ground ambulance: The NSA explicitly excludes ground ambulance. Several states have separate laws.

Free tool

Let the AI check whether your ER bill violates the No Surprises Act.

Upload your ER bill and your EOB. BillBusted identifies whether balance billing protections apply, flags the discrepancy, and generates the exact dispute language — including the CMS complaint link — in about two minutes. Free.

Step-by-step: how to dispute a surprise ER bill

Step 1: Do not pay the bill yet

Paying a bill — even a partial payment — can be treated as accepting the amount. Before writing a check or entering a card number, complete the verification steps above and compare the bill to your EOB.

Step 2: Contact the out-of-network provider in writing

Send a written letter (certified mail, return receipt) stating that you believe the balance bill violates the No Surprises Act, citing your date of service, the emergency nature of the visit, and your in-network insurer. State that you will pay your in-network cost-sharing amount and request a corrected statement. BillBusted's Resolution Pack ($29) includes a ready-to-use dispute letter with NSA-specific language.

Step 3: Notify your insurer

Call the member services number on your insurance card and report the balance-billing situation. Ask your insurer to contact the provider directly. Insurers have financial and legal incentives to enforce NSA protections — the law requires them to pay the out-of-network provider directly, leaving you responsible only for your cost-sharing amount.

Step 4: File a complaint

If steps 2 and 3 do not resolve the issue within 30 days, file a federal complaint (see below).

The exact complaint route

The primary complaint channel for No Surprises Act violations is CMS (Centers for Medicare and Medicaid Services):

- CMS No Surprises Help Desk: cms.gov/nosurprises — file online or call 1-800-985-3059.

- State Department of Insurance: For fully insured plans regulated by your state, also file a parallel complaint with your state DOI. CMS maintains a list of which states have been approved to enforce NSA rules directly.

- Department of Labor EBSA: For employer self-funded plans (ERISA), file at askebsa.dol.gov.

- CFPB: If the bill has been sent to collections or is affecting your credit, file a complaint at consumerfinance.gov/complaint.

Keep copies of everything you submit. CMS has the authority to impose civil monetary penalties on providers that violate the NSA, so complaints are taken seriously.

Research published in JAMA Health Forum found that 74% of patients who dispute a medical bill receive a correction or reduction, making formal complaints and disputes well worth pursuing.

What about that consent form you signed?

Many patients worry that a financial-responsibility consent form or an assignment-of-benefits form signed at ER intake will prevent them from disputing a balance bill. In most cases, it will not.

The No Surprises Act specifically prohibits providers from obtaining a waiver of balance-billing protections for emergency services. A general admission consent form does not constitute a valid waiver of your NSA rights. The only valid waiver under the NSA is a specific, signed document that names the out-of-network provider, states the estimated out-of-network cost, and is provided to the patient in advance — not at intake during an emergency.

If you believe you were pressured to sign away your rights, mention this in your CMS complaint.

For situations involving out-of-network anesthesiologists specifically, see our companion guide: The anesthesiologist was out-of-network. Do I have to pay?

FAQ

Common questions about surprise ER bills

Does the No Surprises Act cover every emergency room visit?

The No Surprises Act applies to emergency services at nearly all hospital ERs and freestanding emergency centers that participate in Medicare. Fully self-funded employer plans that have opted out are a narrow exception, though many states have parallel rules. Up to 49% of medical bills contain at least one error (CFPB, 2023). Review your Explanation of Benefits and call your insurer to confirm your plan type if you receive an unexpected out-of-network balance bill.

What is the maximum a patient owes for out-of-network emergency care under the No Surprises Act?

Under the No Surprises Act, your cost sharing for out-of-network emergency care cannot exceed your in-network amounts. You pay your in-network deductible, copay, and coinsurance and nothing beyond that, regardless of the provider's network status. Up to 49% of medical bills contain at least one error (CFPB, 2023), and balance bills that violate this limit are among the most significant errors patients can dispute. Contact your insurer immediately if you are charged more.

Can a patient dispute an ER balance bill after signing a financial responsibility waiver?

A financial responsibility waiver signed at intake does not override the No Surprises Act. Federal law specifically prohibits providers from asking patients to waive their balance-billing rights during an emergency. Research shows 73.7% of patients who formally dispute a bill receive a correction (JAMA Health Forum, 2024). If you were billed above your in-network cost-sharing amount, contact your insurer and file a complaint regardless of any waiver you signed.

Can a surprise ER bill arrive even when the hospital is in-network?

Yes, a surprise ER bill can still arrive from an in-network hospital when individual physicians such as the emergency medicine group, anesthesiologist, or radiologist are out-of-network. The No Surprises Act covers those out-of-network providers too, so you should only owe your in-network cost-sharing amount. Up to 49% of medical bills contain at least one error (CFPB, 2023), and balance bills from in-network facilities are among the most common ones patients overlook.

Where should a patient file a complaint about an illegal surprise ER bill?

To dispute a surprise ER bill, file a complaint with CMS through its No Surprises Help Desk, which handles most plan types. For fully insured plans, also file with your state Department of Insurance. For employer self-funded ERISA plans, contact the Department of Labor EBSA. Research shows 73.7% of patients who dispute a bill receive a correction (JAMA Health Forum, 2024). Filing in parallel with both federal and state agencies tends to produce the fastest result.

Got a surprise ER bill right now?

Upload the bill and your EOB. BillBusted checks for No Surprises Act violations, flags the discrepancy, and gives you the exact dispute language and complaint link — free, no account needed.